Get Maine Rew 5 Template in PDF

Similar forms

The IRS Form 8288 is similar to the Maine REW-5 form in that both are used to address withholding requirements related to real estate transactions. Form 8288 is specifically for foreign persons selling U.S. real property interests. Like the REW-5, it allows sellers to apply for a reduction or exemption from withholding based on their specific circumstances. Both forms require detailed information about the property, the seller, and the transaction, ensuring that tax obligations are appropriately managed in light of the sale.

Form 1099-S, used for reporting the sale or exchange of real estate, shares similarities with the Maine REW-5 form. Both documents involve the transfer of property and require information about the seller, buyer, and sale price. While the REW-5 focuses on withholding exemptions, Form 1099-S is concerned with reporting the transaction to the IRS. This reporting is essential for tax purposes, and both forms aim to ensure compliance with federal and state tax laws.

The California Form 593 is another document akin to the Maine REW-5. It is utilized for reporting real estate withholding in California. Like the REW-5, Form 593 allows sellers to request a reduction or exemption from withholding based on their tax situation. Both forms require the seller to provide information about their ownership and the property being sold, ensuring that tax withholding aligns with the seller's actual tax liability.

Moreover, understanding the importance of proper documentation extends to various forms used in real estate transactions, including the Maine REW-5. For businesses, having a well-structured approach to their documents can be crucial; for instance, the PDF Templates provide essential guidance and templates to facilitate the creation of important forms, such as the Employee Handbook. This ensures that both companies and their employees are clear on expectations and legal obligations.

The New York State Form IT-2663 serves a similar purpose to the Maine REW-5, focusing on withholding tax on the sale of real property by non-residents. This form allows sellers to request a reduced withholding amount or exemption. Both forms require detailed information about the seller, the property, and the nature of the sale, helping to accurately determine the appropriate tax withholding amount based on the seller's circumstances.

The Florida Form DR-219 is comparable to the Maine REW-5 in that it addresses real estate withholding for non-residents. This form allows sellers to apply for a withholding certificate, similar to the exemption process in Maine. Both forms are designed to ensure that sellers are not overburdened by tax withholding that exceeds their actual tax liability, requiring them to provide supporting documentation regarding the sale and ownership of the property.

The Texas Form 50-284 is another document that resembles the Maine REW-5. It is used to request a reduction in withholding for non-resident sellers of Texas real estate. Like the REW-5, this form requires detailed information about the property, the seller, and the transaction. Both forms aim to ensure that tax withholding is fair and reflects the seller's actual tax obligation, preventing unnecessary financial strain during the closing process.

The Massachusetts Form 1-NR/PY is similar to the Maine REW-5 in that it addresses withholding for non-resident sellers of real estate. This form allows sellers to report their income and request a reduction in withholding. Both forms require comprehensive information about the seller and the property being sold, ensuring compliance with tax laws while allowing for adjustments based on individual circumstances.

The Illinois Form CRT-1 is akin to the Maine REW-5, as it is used for real estate withholding for non-residents. Sellers can apply for a reduced withholding amount based on their specific tax situations. Both forms require detailed information about the seller, the property, and the transaction, allowing tax authorities to accurately assess the appropriate withholding amount based on the seller’s actual tax liability.

The Virginia Form 763 is another document that parallels the Maine REW-5. It is used for withholding tax on the sale of real estate by non-residents. Like the REW-5, this form allows sellers to apply for a withholding exemption or reduction. Both forms require sellers to provide extensive information about the sale and their ownership of the property, ensuring that tax withholding is aligned with the seller's actual tax obligations.

Finally, the Washington State Form 2 is similar to the Maine REW-5 as it pertains to real estate withholding for non-residents. This form allows sellers to request an exemption or reduction in withholding based on their circumstances. Both forms emphasize the importance of providing detailed information about the property and the seller, helping to ensure that tax withholding is fair and accurately reflects the seller’s tax liability.

Misconceptions

Understanding the Maine REW-5 form is essential for anyone involved in the sale of real property in Maine. However, several misconceptions can lead to confusion. Here are five common misconceptions:

- Only residents of Maine can file the REW-5 form. In reality, the form is specifically designed for sellers who are nonresidents of Maine. This means that anyone selling Maine real estate, regardless of their residency status, can utilize this form to request an exemption or reduction in withholding.

- Submitting the REW-5 form is optional. While it may seem like a simple formality, submitting the REW-5 form is crucial for sellers who want to avoid excessive withholding on their sales. It must be submitted no fewer than five business days prior to closing to ensure proper processing.

- The REW-5 form guarantees a tax exemption. It’s a common belief that filling out the form automatically results in a tax exemption. However, the Maine Revenue Services may require additional documentation and will review each request before granting any exemptions or reductions in withholding.

- All sellers need to fill out the REW-5 form individually. This is not entirely true. If there are multiple sellers who are married and plan to file a joint Maine individual income tax return, they can complete one form together. They simply need to list both names and Social Security Numbers on the same form.

- Closing costs can be arbitrarily calculated. Many people think they can estimate closing costs without proper documentation. However, the form requires specific allowable closing costs from the original purchase, and these must be accurately calculated based on the provided guidelines.

By addressing these misconceptions, individuals can better navigate the process of completing the Maine REW-5 form and ensure compliance with state tax regulations.

Popular PDF Documents

Maine Motor Vehicle - It is also needed when there are questions about a vehicle's VIN.

For those seeking to understand the process better, a thorough guide on utilizing the Quitclaim Deed in Ohio transactions can be invaluable, offering insights into its applications and nuances.

Motion to Enforce - The motion must be filed in the appropriate district court in Maine.

Documents used along the form

The Maine REW-5 form serves as a critical tool for sellers of real property in Maine who wish to request an exemption or reduction in the withholding of state income tax. However, this form is often accompanied by several other documents that are essential for a smooth transaction. Below is a list of these forms and documents, each playing a unique role in the process.

- Form 2848-ME (Power of Attorney): This document allows a seller to designate an individual to represent them in discussions with Maine Revenue Services. It grants the representative authority to receive confidential information related to the seller’s tax records.

- Purchase and Sale Agreement: This is a legally binding contract between the buyer and seller outlining the terms of the sale, including the purchase price and closing date. It is essential for establishing the transaction details.

- HUD-1 Settlement Statement: This form provides a detailed account of all costs associated with the sale of the property. It includes closing costs and is typically used in real estate transactions to ensure transparency.

- Real Estate Transfer Tax Declaration (RETTD): This document is filed with the state to report the transfer of real estate and is often required for tax purposes. It helps in determining the tax liability related to the sale.

- Appraisal Report: If the property was inherited, an appraisal report may be necessary to establish its fair market value at the time of the decedent’s death. This information is crucial for tax calculations.

- Tax Assessment Records: These documents provide information about the assessed value of the property, which can be useful in determining the basis for capital gains calculations.

- Closing Statement: Similar to the HUD-1, this document outlines the financial settlement between the buyer and seller. It details all fees, credits, and debits involved in the transaction.

- List of Capital Improvements: Sellers must provide documentation of any capital improvements made to the property, as these can affect the basis for tax calculations. Receipts and contracts can serve as proof.

- Depreciation Schedule: If the property was used for rental or commercial purposes, a depreciation schedule detailing accumulated depreciation may be required for accurate tax reporting.

- California Motorcycle Bill of Sale: This essential document records the ownership transfer of a motorcycle, detailing information such as the motorcycle's identification number, sale price, and parties involved. To learn more, visit My PDF Forms.

- IRS Publication 523: This publication offers guidance on selling a home, including how to report the sale, determine basis, and understand capital improvements. It is a valuable resource for sellers navigating tax implications.

Understanding these documents can significantly ease the process of selling real estate in Maine. Each form plays a vital role in ensuring compliance with tax regulations and facilitating a smooth transaction. Sellers should prepare these documents carefully to avoid delays and complications during the closing process.

Form Preview Example

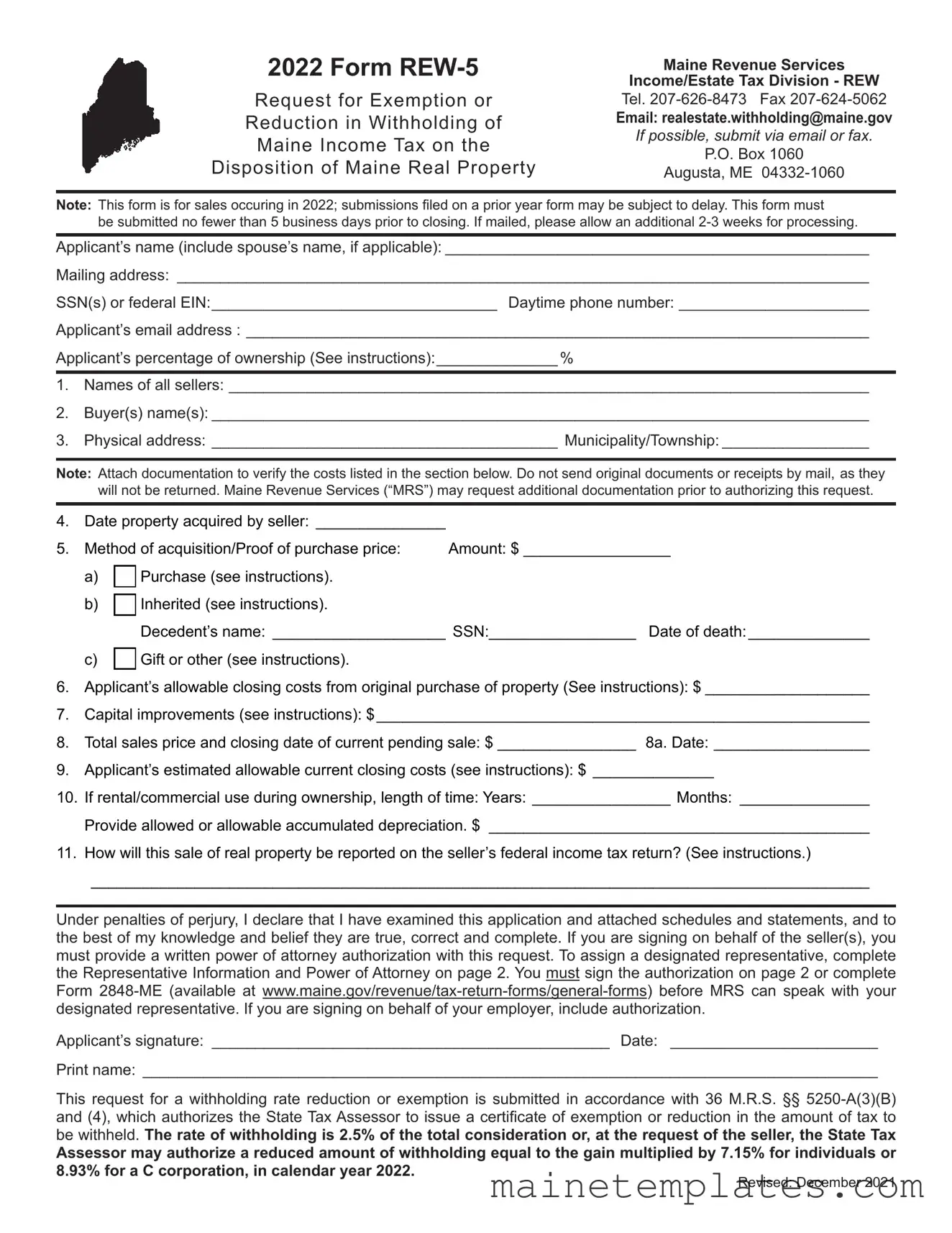

2022 Form

Request for Exemption or Reduction in Withholding of Maine Income Tax on the Disposition of Maine Real Property

Maine Revenue Services

Income/Estate Tax Division - REW

Tel.

Email: realestate.withholding@maine.gov

If possible, submit via email or fax.

P.O. Box 1060

Augusta, ME

Note: This form is for sales occuring in 2022; submissions filed on a prior year form may be subject to delay. This form must

be submitted no fewer than 5 business days prior to closing. If mailed, please allow an additional

Applicant’s name (include spouse’s name, if applicable): _________________________________________________

Mailing address: ________________________________________________________________________________

SSN(s) or federal EIN:_________________________________ Daytime phone number: ______________________

Applicant’s email address : ________________________________________________________________________

Applicant’s percentage of ownership (See instructions):______________ %

1.Names of all sellers: __________________________________________________________________________

2.Buyer(s) name(s): ____________________________________________________________________________

3.Physical address: ________________________________________ Municipality/Township: _________________

Note: Attach documentation to verify the costs listed in the section below. Do not send original documents or receipts by mail, as they will not be returned. Maine Revenue Services (“MRS”) may request additional documentation prior to authorizing this request.

4. |

Date property acquired by seller: _______________ |

|

||

5. |

Method of acquisition/Proof of purchase price: |

Amount: $ _________________ |

||

|

a) |

|

Purchase (see instructions). |

|

|

|

|

||

|

|

|

|

|

|

b) |

|

Inherited (see instructions). |

|

|

|

|

Decedent’s name: ____________________ SSN:_________________ Date of death:______________ |

|

c)

Gift or other (see instructions).

Gift or other (see instructions).

6.Applicant’s allowable closing costs from original purchase of property (See instructions): $ ___________________

7.Capital improvements (see instructions): $_________________________________________________________

8.Total sales price and closing date of current pending sale: $ ________________ 8a. Date: __________________

9.Applicant’s estimated allowable current closing costs (see instructions): $ ______________

10.If rental/commercial use during ownership, length of time: Years: ________________ Months: _______________

Provide allowed or allowable accumulated depreciation. $ ____________________________________________

11.How will this sale of real property be reported on the seller’s federal income tax return? (See instructions.)

__________________________________________________________________________________________

Under penalties of perjury, I declare that I have examined this application and attached schedules and statements, and to the best of my knowledge and belief they are true, correct and complete. If you are signing on behalf of the seller(s), you must provide a written power of attorney authorization with this request. To assign a designated representative, complete the Representative Information and Power of Attorney on page 2. You must sign the authorization on page 2 or complete Form

Applicant’s signature: ______________________________________________ Date: ________________________

Print name: _____________________________________________________________________________________

This request for a withholding rate reduction or exemption is submitted in accordance with 36 M.R.S. §§

be withheld. The rate of withholding is 2.5% of the total consideration or, at the request of the seller, the State Tax

Assessor may authorize a reduced amount of withholding equal to the gain multiplied by 7.15% for individuals or 8.93% for a C corporation, in calendar year 2022.

Revised: December 2021

Representative Information (complete only if you want someone to represent you during the real estate withholding process)

Representative name (and title, if applicable)

Firm or company name

Mailing address

City, state, zip

Country (if not United States)

Email address

Telephone number

Limited Power of Attorney (complete only if you want someone to represent you during the real estate withholding process)

By signing below, the selling party appoints the individual named in the above section to act as their representative with authority to receive confidential information and to discuss your tax records, related to this form, with MRS. I understand

that my representative may not act on my behalf, unless I provide a Form

Seller signature

Print name (and title, if applicable)

Date

Additional seller signature (if applicable)

Print name (and title, if applicable)

Date

General Instructions

Purpose of Form: To request an exemption or reduction in withholding of Maine income tax on the disposition of Maine real property.

Who may File: A seller (individual, firm, partnership, association, society, club, corporation, estate, trust, business trust, receiver, assignee or any other group or combination acting as a unit) of Maine real property who, at the time of closing, is a nonresident of Maine.

Withholding Certificate Issued by the State Tax Assessor: A withholding certificate may be issued by the

State Tax Assessor to reduce or eliminate withholding on transfers of Maine real property interests by nonresidents.

The certificate may be issued if:

1.No tax is due on the gain from the transfer; or,

2.Reduced withholding is appropriate because the 2.5% amount exceeds the seller’s maximum Maine income tax liability on the gain realized from the sale. The maximum income tax liability is equal to the seller’s capital gain multiplied by 7.15% (8.93% for corporations).

If one of the above is applicable, apply for the certificate no later than five business days prior to closing. Do not apply if

the maximum Maine income tax liability exceeds 2.5% of the consideration.

Foreclosure Sale: If property is subject to foreclosure and the consideration received for the property does not exceed the debt secured by that property, no Maine income tax withholding is required. Foreclosure sale means a sale of real property incident to a foreclosure and includes a mortgagee’s sale of real estate owned property of which the mortgagee, or

of a previous foreclosure auction. MRS does not issue withholding exemption certificates for this type of foreclosure

sale (see Rule 803 and 36 M.R.S. §

2

Specific Instructions

Email Form

Applicant’s name: Enter the applicant’s (seller’s) name.

NOTE: If there are multiple sellers of the property, each

applicant (seller) must complete a separate Form REW-

5, except that married taxpayers that will file a joint Maine individual income tax return requesting a withholding exemption or reduction may complete one form, listing both names and SSN’s on the form.

Mailing address: Enter the applicant’s current mailing address.

Social Security Number (SSN) or Employer Identification

Number (EIN): Enter the SSN or EIN of the applicant listed on this form. If applicable, enter your spouse’s SSN.

Line 1. If applicant’s ownership percentage is less than 100%, all sellers must be listed on this line. The seller(s) are typically listed on the Purchase and Sale Agreement. Attach additional pages, if necessary.

Line 2. Enter the names(s) of the buyer(s). The buyers are typically listed on the Purchase and Sale Agreement. Attach additional pages, if necessary.

Line 3. Enter the physical address of the property being sold.

Line 4. Enter the date the seller acquired the property.

Line 5. Indicate the method by which the seller obtained ownership of the property.

a)If you purchased the property, attach verification of the original sales price, such as

b)If you inherited the property, provide a complete appraisal dated within six months of the decedent’s death or a copy of the tax assessment from the town. Enter the decedent’s name, SSN and the date of death in the spaces provided.

c)If you received the property as a gift, provide documents to verify the original purchase price paid by the previous owner. If you cannot locate these documents, the town where the property is located may have a record of the purchase price. As a general rule, for purposes of determining the gain, you will use the donor’s adjusted basis at the time of gift as your basis.

Line 6. Enter the amount of the allowable original closing costs you paid at the time of acquisition*. Also see line 9.

Line 7. Provide a list of capital improvements made to the home along with the cost of each improvement. Do

not include repairs made to the property. For example:

Cleaning or fixing a furnace is not a capital improvement, but installing a new furnace is. If you built the home, provide the information for the build. You can make a detailed list of the items purchased (including the cost of each and providing

receipts), provide a copy of the contract with the builder, provide the building permit filed with the town, or provide the tax assessment from the year you received the certification

of occupancy. Attach additional pages as needed.

Line 8. Enter the total gross sales price of the property. Do not subtract any fees. The sale price should match the sales price on the Purchase and Sales Agreement. If there are multiple sellers, list this seller’s ownership percentage.

Line 8a. Enter the closing date for the sale of this property.

Line 9. Enter the amount of the applicant’s allowable closing costs from the current sale of this property*. Also see line 6.

*Certain closing costs do not qualify. If available, enclose a copy of the

For more information about selling your home, determining basis, reporting the sale, capital improvements and costs, see IRS Publication 523.

Line 10. If the property was rented or used commercially, enter the allowed, or allowable, accumulated depreciation determined in accordance with the Internal Revenue Code.

Line 11. Indicate whether the sale will be reported as a gain, loss, exclusion, installment sale or

Representative Information & Limited Power of Attorney

Although not required, you may designate someone to represent you during the real estate withholding process. To do so, complete the Representative Information and Limited Power of Attorney sections on page 2 of Form

designated representative must be an individual, although a firm cannot be designated as your representative, an individual of a firm can be.

Appointing a Limited Power of Attorney designates a representative to receive confidential information and to discuss tax records related to your Form

with MRS. The designated representative may not act on your behalf, unless a completed Form

3

File Attributes

| Fact Name | Description |

|---|---|

| Form Purpose | This form is used to request an exemption or reduction in withholding of Maine income tax on the sale of Maine real property. |

| Governing Law | The form is governed by 36 M.R.S. §§ 5250-A(3)(B) & (4), which empower the State Tax Assessor to issue certificates regarding tax withholding. |

| Submission Deadline | The form must be submitted at least five business days prior to the closing date to ensure processing. |

| Contact Information | For inquiries, contact Maine Revenue Services at 207-626-8473 or via email at realestate.withholding@maine.gov. |

| Withholding Rate | The standard withholding rate is 2.5% of the total consideration, but sellers can request a reduced rate based on their gain. |

| Additional Documentation | Maine Revenue Services may require additional documentation before granting an exemption or reduction in withholding. |

| Who May File | Any seller of Maine real property who is a nonresident at the time of closing can file this form. |

| Power of Attorney | To designate a representative, sellers must complete the Power of Attorney section on the form or provide Form 2848-ME. |

Detailed Guide for Using Maine Rew 5

Completing the Maine REW-5 form requires careful attention to detail to ensure all necessary information is accurately provided. Following these steps will help facilitate the process and avoid delays. After filling out the form, it should be submitted via email or fax to the Maine Revenue Services. It is essential to submit the form at least five business days prior to closing to allow for processing.

- Fill in the Applicant’s Name: Enter the full name of the applicant, including the spouse’s name if applicable.

- Provide Mailing Address: Enter the current mailing address of the applicant.

- Enter Social Security Number or EIN: Fill in the SSN or federal EIN for the applicant. Include the spouse’s SSN if applicable.

- Daytime Phone Number: Provide a contact number where the applicant can be reached during business hours.

- Applicant’s Email Address: Enter the email address of the applicant or the designated Power of Attorney.

- Ownership Percentage: Indicate the applicant’s percentage of ownership in the property.

- List Names of All Sellers: Write the names of all sellers involved in the transaction.

- Enter Buyer(s) Name(s): Fill in the names of the buyers as listed in the Purchase and Sale Agreement.

- Property Information: Provide the physical address of the property, including map, block, lot, and sub-lot numbers.

- Date Property Acquired: Enter the date when the seller acquired the property.

- Method of Acquisition: Indicate how the seller obtained the property and provide the necessary documentation.

- Allowable Closing Costs: Enter the total amount of allowable closing costs from the original purchase of the property.

- Capital Improvements: List any capital improvements made to the property and their costs.

- Total Sales Price: Provide the total sales price of the current pending sale.

- Estimated Allowable Closing Costs: Enter the estimated allowable closing costs for the current sale.

- Rental/Commercial Use: If applicable, indicate the length of time the property was used for rental or commercial purposes and provide accumulated depreciation.

- Reporting on Tax Return: Explain how the sale will be reported on the seller’s federal income tax return.

- Signature: The applicant must sign and date the form, certifying the information provided is true and correct.