Get Maine Tax Template in PDF

Similar forms

The Maine Real Estate Transfer Tax Declaration (Form RETTD) shares similarities with the IRS Form 1099-S, which is used for reporting the sale of real estate. Both documents require detailed information about the parties involved in the transaction, including the seller and buyer's names and addresses. Additionally, they both capture the sale price of the property and the date of transfer. The 1099-S, however, is specifically focused on reporting income for tax purposes, while the Maine RETTD is primarily concerned with assessing transfer taxes based on the property's value.

Another document comparable to the Maine Tax form is the HUD-1 Settlement Statement. This form is used in real estate transactions to outline the costs and fees associated with the sale of property. Like the RETTD, the HUD-1 requires detailed information about the buyer and seller, as well as the property being transferred. Both documents aim to provide transparency in real estate transactions. However, the HUD-1 goes further by itemizing all financial aspects of the transaction, such as loan fees and closing costs, which the RETTD does not address directly.

The Quitclaim Deed is also similar to the Maine Tax form in that it involves the transfer of property ownership. This document allows a seller to transfer any interest they have in a property to the buyer without guaranteeing that the title is clear of any claims. While the RETTD focuses on tax implications and the details of the transaction, the Quitclaim Deed serves as a legal instrument that formalizes the transfer of property rights. Both documents require identification of the parties involved and details about the property, but they serve different legal purposes.

In addition to these important documents, the Employment Verification Form plays a significant role in confirming job history and employment details, much like the various forms discussed. Having reliable verification can streamline real estate transactions as potential buyers often need to showcase their financial stability. To ensure the necessary documentation is readily available, you may want to utilize the PDF Templates for easy access to the appropriate forms.

Another relevant document is the Deed of Trust, which is often used in real estate transactions to secure a loan. Similar to the Maine Tax form, the Deed of Trust includes information about the borrower, lender, and the property involved. Both documents are essential in the context of real estate, as they outline the terms of the transaction and the responsibilities of the parties. However, the Deed of Trust specifically relates to financing and collateral, while the RETTD is focused on tax obligations arising from the transfer of property ownership.

Lastly, the Property Tax Assessment Form bears resemblance to the Maine Tax form in that it involves property details and valuation. This form is used by local governments to assess property taxes based on the value of real estate. Like the RETTD, it requires information about the property location, ownership, and type. However, the Property Tax Assessment Form is primarily concerned with determining the annual tax liability, while the RETTD is focused on the one-time transfer tax that occurs during the sale of the property.

Misconceptions

Understanding the Maine Tax form can be challenging, and several misconceptions often arise. Here are nine common misunderstandings about the Maine Real Estate Transfer Tax Declaration (Form RETTD) and clarifications to help you navigate the process effectively.

- Misconception 1: The transfer tax only applies to sales of property.

- Misconception 2: Only the buyer is responsible for the transfer tax.

- Misconception 3: You can use red ink on the form.

- Misconception 4: You do not need to file the form if the property is in multiple municipalities.

- Misconception 5: The fair market value must always be provided.

- Misconception 6: The property type code is optional.

- Misconception 7: You can skip the declaration under penalty of perjury.

- Misconception 8: If the seller is a Maine resident, no income tax withholding is necessary.

- Misconception 9: The form can be submitted after the deed is recorded.

This is incorrect. The transfer tax also applies to gifts of property. If the transfer is a gift, you should enter "0" for the purchase price on the form.

Both the buyer and seller share the responsibility for the transfer tax. The tax is divided equally between the two parties, making it essential for both to be aware of the tax implications.

Using red ink is not permitted. The form must be completed in black or blue ink to ensure clarity and proper processing.

If the property spans multiple municipalities, you must complete a Supplemental Form for each additional municipality. Failing to do so can lead to delays or penalties.

You only need to enter the fair market value if you reported "0" or a nominal amount for the purchase price. Otherwise, this line can be left blank.

The property type code is mandatory. You must select the code that best describes the property being transferred to ensure accurate tax calculation.

This declaration is crucial. It affirms that the information provided is true and complete. Neglecting this section can lead to legal consequences.

While Maine residents are generally exempt from withholding, certain conditions apply. It's essential to review the specific exemptions listed on the form.

The form must be filed simultaneously with the deed at the county Registry of Deeds. Delaying this can result in complications with the property transfer.

Addressing these misconceptions can streamline your experience with the Maine Tax form and ensure compliance with local regulations. Always refer to the latest instructions or consult with a professional if you have questions.

Popular PDF Documents

Maine Advance Directive Form - This form allows you to designate an agent to make health care decisions for you when you're unable.

A Colorado Non-disclosure Agreement (NDA) is a legal contract designed to protect sensitive information shared between parties. This form establishes the confidentiality obligations of the parties involved, ensuring that proprietary information remains secure. Understanding the nuances of this agreement is essential for anyone looking to safeguard their business interests in Colorado, especially when utilizing a well-drafted Confidentiality Agreement.

Maine Drivers Permit - One document must show your date of birth; the other must bear your signature.

Documents used along the form

When engaging in real estate transactions in Maine, several forms and documents accompany the Maine Tax form, specifically the Real Estate Transfer Tax Declaration (Form RETTD). These documents serve various purposes, ensuring compliance with state regulations and facilitating the smooth transfer of property ownership. Below is a list of commonly used forms and documents that may be required alongside the Maine Tax form.

- Deed: This legal document formally transfers ownership of the property from the seller to the buyer. It includes essential details such as the names of the parties involved, a description of the property, and any conditions of the sale.

- Supplemental Form: Required when there are multiple buyers or sellers, this form provides additional information necessary for the Registry of Deeds to process the transaction accurately.

- Property Tax Maps: These maps help identify the specific location and boundaries of the property being transferred. They are crucial for determining property classifications and tax assessments.

- Exemption Claim Form: If either the buyer or seller claims an exemption from the transfer tax, this form must be completed to explain the basis for the exemption, as outlined in Maine law.

- Income Tax Withholding Form: Nonresident sellers may need to submit this form to report any income tax withholding required on the sale of the property, ensuring compliance with state tax laws.

- Affidavit of Title: This document certifies that the seller has clear title to the property and has the legal right to sell it. It protects the buyer from potential claims against the property.

- Closing Disclosure: This form outlines the final terms of the mortgage, including the loan amount, interest rate, and all closing costs. It ensures that both parties are aware of their financial obligations.

- Residential Lease Agreement Form: For those entering into rental agreements, the detailed Residential Lease Agreement terms and conditions clarify the rights and responsibilities of both tenants and landlords.

- Purchase Agreement: This contract details the terms of the sale, including the purchase price, contingencies, and timelines. It serves as a binding agreement between the buyer and seller.

- Title Insurance Policy: This insurance protects the buyer and lender from any title defects or disputes that may arise after the purchase, providing peace of mind regarding ownership rights.

- Home Inspection Report: Although not always required, this report provides an assessment of the property's condition, highlighting any issues that may affect its value or safety.

Each of these documents plays a vital role in the real estate transaction process in Maine. Understanding their purposes can help ensure a smoother experience for all parties involved. It is always advisable to consult with a qualified professional to navigate these requirements effectively.

Form Preview Example

|

|

|

MAINE REAL ESTATE |

|

|

|

|

|

|

00 |

TRANSFER TAX DECLARATION |

|

|

Form RETTD |

|

|

*18RETTD* |

|

|

|

|

|

|

|

|

|

Do not use red ink. |

|

|

|

|

1.County

2.Municipality

3.GRANTEE/PURCHASER

3a. Last name, fi rst name, MI; or business name

3c. Last name, fi rst name, MI; or business name

3e. Mailing address after purchasing this property |

3f. Municipality |

|

|

|

|

BOOK/PAGE - REGISTRY USE ONLY

3b. Federal ID

3d. Federal ID

3g. State 3h. ZIP Code

4. GRANTOR/SELLER

|

4a. Last name, fi rst name, MI; or business name |

|

|

4b. |

Federal ID |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4c. Last name, fi rst name, MI; or Business name |

|

|

|

|

|

|

|

|

|

|

|

4d. |

Federal ID |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4e. Mailing address |

4f. Municipality |

4g. |

State 4h. ZIP Code |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. PROPERTY 5a. Map |

|

Block |

|

Lot |

|

Check any that apply |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

No maps exist |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Multiple parcels |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

5c. Physical location |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Portion of parcel |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Not applicable |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5b. Type of property - enter the code number that best describes the prop- erty being sold (see instructions).

5d. Acreage (see instructions)

.

6. TRANSFER TAX |

6a. |

Purchase price (If the transfer is a gift, enter “0”) |

6a. |

|

|

.00 |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

||

|

6b. |

Fair market value (Enter a value only if you entered “0” or a nominal value on line 6a) |

6b. |

|

|

||

|

|

|

|

|

|

|

|

6c. Exemption claim -  Check the box if either grantor or grantee is claiming exemption from transfer tax and enter explanation below.

Check the box if either grantor or grantee is claiming exemption from transfer tax and enter explanation below.

7. DATE OF TRANSFER |

8. CLASSIFIED. WARNING TO BUYER - If the property is classifi ed as farmland, |

|

|

||

open space, tree growth, or working waterfront, a substantial fi nancial penalty may |

|

|

|||

|

|

|

|

CLASSIFIED |

|

|

|

|

|

||

|

|

|

|

||

|

|

|

|

||

|

|

|

be triggered by development, subdivision, partition, or change in use. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9.SPECIAL CIRCUMSTANCES. Were there any special circumstances with

the transfer that suggest the price paid was either more or less than its fair market value? If yes, check the box and enter explanation below.

10.INCOME TAX WITHHELD. The buyer is not required to withhold Maine income tax because:

Seller has qualified as a Maine resident

Seller has qualified as a Maine resident

A waiver has been received from the State Tax Assessor

A waiver has been received from the State Tax Assessor

Consideration for the property is less than $100,000

Consideration for the property is less than $100,000  The transfer is a foreclosure sale

The transfer is a foreclosure sale

11.DECLARATION(S) UNDER THE PENALTIES OF PERJURY. I declare that I have examined this return/report/document and (if applicable) accompanying schedules and statements and to the best of my knowledge and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

PREPARER. Name of preparer: _____________________________________ Phone number:

__________________________________________

Mailing address: ______________________________________________ Email address: ___________________________________________

______________________________________________ Fax number:_____________________________________________

Rev. 11/21

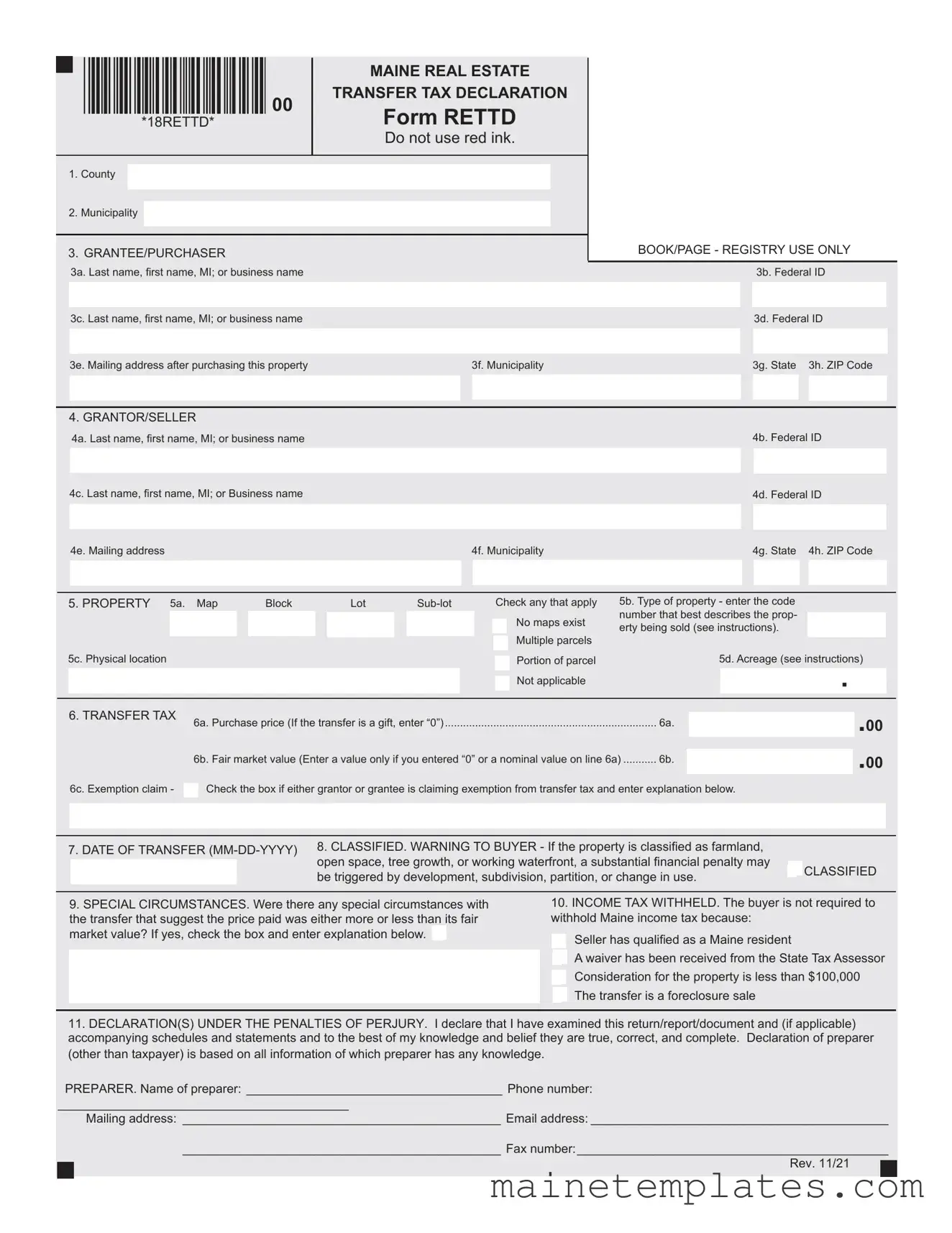

Real Estate Transfer Tax Declaration

Instructions

The Real Estate Transfer Tax Declaration (Form RETTD) must be fi led with the county Registry of Deeds when the accompanying deed is recorded. The Registry of Deeds will collect a tax based on the value of the transferred property. The tax is equals $2.20 for each $500 of value and is imposed half on the purchaser and half on the seller. If the transferred property is in more than one municipality or if there are more than two sellers or buyers, a Supplemental Form must be completed. For more information, visit www.maine.gov/ revenue/propertytax/transfertax/transfertax.htm or contact the Property Tax Division at

Line 1. County. Enter the name of the county where the property is lo- cated. If the property is in more than one county, complete separate Forms

RETTD.

Line 2. Municipality. Enter the name of the municipality where the prop- erty is located. If the transferred property is located in more than one mu- nicipality, complete a Supplemental Form.

Line 3. Grantee/Purchaser. a) & c): Enter one name on each available line, beginning with last name fi rst. If more than two purchasers, complete a Supplemental Form. b) & d): If a business entity is entered on a) or c), enter the entity’s federal ID number. Do not enter a social security number. If you do not have a federal ID number, or if the transfer is of unimproved land for less than $25,000 or land with improvements for less than $50,000, you may enter all 0s in this fi eld. e) through h): Enter the mailing address for the buyer after the purchase of this property.

Line 4. Grantor/Seller. a) & c): Enter one name on each available line, beginning with last name fi rst. If more than two sellers, complete a Supplemental Form. b) & d): If a business entity is entered on a) or c), enter the entity’s federal ID number. Do not enter a social security number If you do not have a federal ID number, or if the transfer is of unimproved land for less than $25,000 or land with improvements for less than $50,000, you may enter all 0s in this fi eld. e) through h): Enter the mailing address for the seller after the purchase of this property.

Line 5. Property. a): Enter the appropriate

don’t know the exact acreage, enter an estimate based on the available information. The acreage recital is for MRS purposes only and it does not constitute a guarantee to the buyer of the acreage being conveyed. EXCEPTION: If the transferred property is a gift, you do not need to complete lines b) and d).

Line 6. Transfer tax. a): Enter the actual sale price or “0” if the transfer

is a gift. b): If you entered 0 or a sale price that is considered nominal on line a), enter the fair market value of the property on this line. The fair market value is based on the estimated price a property will bring in the open market and under prevailing market conditions in a sale between a willing buyer and a willing seller and must reflect the value at the time of the transfer. c): If either party is claiming an exemption from the transfer tax, check this box and enter an explanation of the reason for the claim. See 36 M.R.S. §

Line 7. Date of transfer. Enter the date of the property transfer, which refl ects when the ownership or title to the real property is delivered to the purchaser. This date may not be the same as the recording date.

Line 8. Classified. Check the box if the property is enrolled in one of the current use programs. Current use programs are tree growth, farm and open space, and working waterfront.

Line 9. Special circumstances. If the sale of the property was either substantially more or less than the fair market value, check this box and enter an explanation of the circumstances.

Line 10. Income tax withheld. Nonresident sellers are subject to real estate withholding under 36 M.R.S. §

Line 11. Declaration(s) under penalty of perjury. Please provide the name, mailing address, phone number, and email address of the person or company preparing this form if diff erent from the parties of the transaction.

PROPERTY TYPE CODES

VACANT LAND |

|

COMMERCIAL |

|

INDUSTRIAL |

|

RESIDENTIAL |

|

MISC CODES |

|

Rural |

101 |

Mixed use |

301 |

Gas and oil |

401 |

Rural |

201 |

Government |

501 |

Urban |

102 |

5+ unit apt. |

303 |

Utility |

402 |

Urban |

202 |

Condominium |

502 |

Oceanfront |

103 |

Bank |

304 |

Gravel pit |

403 |

Oceanfront |

203 |

Timeshare unit |

503 |

Lake/pond front |

104 |

Restaurant |

305 |

Lumber/saw mill |

404 |

Lake/pond front |

204 |

Nonprofi t |

504 |

Stream/riverfront |

105 |

Medical |

306 |

Pulp/paper mill |

405 |

Stream/riverfront |

205 |

Mobile home park |

505 |

Agricultural |

106 |

Office |

307 |

Light manufacture |

406 |

Mobile home |

206 |

Airport |

506 |

Commercial zone 107 |

Retail |

308 |

Heavy manufacture |

407 |

207 |

Conservation |

507 |

||

Other |

120 |

Automotive |

309 |

Other |

420 |

Other |

220 |

Current use |

|

|

|

Marina |

310 |

|

|

|

|

classifi cation |

508 |

|

|

Warehouse |

311 |

|

|

|

|

Other |

520 |

|

|

Hotel/motel/inn |

312 |

|

|

|

|

|

|

|

|

Nursing home |

313 |

|

|

|

|

|

|

|

|

Shopping mall |

314 |

|

|

|

|

|

|

|

|

Other |

320 |

|

|

|

|

|

|

File Attributes

| Fact Name | Details |

|---|---|

| Form Name | The form is called the Maine Real Estate Transfer Tax Declaration, known as Form RETTD. |

| Filing Requirement | This form must be filed with the county Registry of Deeds when the deed is recorded. |

| Transfer Tax Rate | The tax rate is $2.20 for every $500 of property value transferred. |

| Tax Division Contact | For questions, you can contact the Property Tax Division at 207-624-5606. |

| Exemption Claims | Exemptions from transfer tax can be claimed under 36 M.R.S. § 4641-C. |

| Special Circumstances | Buyers must indicate if special circumstances affected the transfer price. |

| Income Tax Withholding | Nonresident sellers may be subject to withholding under 36 M.R.S. § 5250-A. |

| Multiple Parties | If there are more than two buyers or sellers, a Supplemental Form is required. |

| Property Classification | Properties classified under certain programs may incur financial penalties if developed. |

Detailed Guide for Using Maine Tax

Filling out the Maine Real Estate Transfer Tax Declaration form is essential when transferring property. This form must be submitted to the county Registry of Deeds along with the deed. Below are the steps to complete the form accurately.

- County: Enter the name of the county where the property is located.

- Municipality: Enter the name of the municipality where the property is located.

- Grantee/Purchaser:

- 3a: Enter the last name, first name, and middle initial (or business name).

- 3b: Enter the federal ID number (if applicable).

- 3c: Enter the last name, first name, and middle initial of any additional purchaser.

- 3d: Enter the federal ID number for the additional purchaser (if applicable).

- 3e: Enter the mailing address after purchasing the property.

- 3f: Enter the municipality.

- 3g: Enter the state.

- 3h: Enter the ZIP code.

- Grantor/Seller:

- 4a: Enter the last name, first name, and middle initial (or business name).

- 4b: Enter the federal ID number (if applicable).

- 4c: Enter the last name, first name, and middle initial of any additional seller.

- 4d: Enter the federal ID number for the additional seller (if applicable).

- 4e: Enter the mailing address for the seller after the property transfer.

- 4f: Enter the municipality.

- 4g: Enter the state.

- 4h: Enter the ZIP code.

- Property:

- 5a: Enter the map-block-lot-sub lot number.

- 5b: Enter the property type code that best describes the property.

- 5c: Enter the physical location if no property tax maps exist.

- 5d: Enter the acreage of the property.

- Transfer Tax:

- 6a: Enter the purchase price or "0" if the transfer is a gift.

- 6b: Enter the fair market value if applicable.

- 6c: Check the box if claiming an exemption and provide an explanation.

- Date of Transfer: Enter the date the property transfer occurs.

- Classified: Check the box if the property is classified under certain programs.

- Special Circumstances: Check the box if there are special circumstances affecting the price and provide an explanation.

- Income Tax Withheld: Indicate the reason the buyer is not required to withhold Maine income tax.

- Declaration: Provide the name, mailing address, phone number, and email address of the preparer if different from the parties involved.