Legal Promissory Note Form for the State of Maine

Similar forms

The Maine Promissory Note is similar to a Loan Agreement. Both documents outline the terms of a loan, including the amount borrowed, interest rate, and repayment schedule. A Loan Agreement may include additional details such as collateral requirements and specific conditions under which the loan must be repaid. While a Promissory Note is often simpler and focuses primarily on the borrower's promise to repay, a Loan Agreement is more comprehensive and legally binding in a broader sense.

Another document that resembles the Maine Promissory Note is a Mortgage. A Mortgage is a specific type of loan secured by real property. Like a Promissory Note, it involves a borrower agreeing to repay a specified amount. However, the Mortgage includes terms related to the property being used as collateral, such as foreclosure rights in case of default. The Promissory Note supports the Mortgage by detailing the borrower's promise to pay back the loan amount.

A Personal Guarantee is also similar to a Promissory Note. This document involves an individual agreeing to take responsibility for another person's debt. It provides a personal assurance to the lender that the debt will be repaid. While a Promissory Note is primarily focused on the loan itself, a Personal Guarantee emphasizes the borrower's accountability, which can provide additional security for the lender.

A Secured Loan Agreement shares similarities with the Maine Promissory Note as well. Both documents involve a borrower receiving funds with an obligation to repay. The key difference lies in the secured nature of the loan, where collateral is specified in the Secured Loan Agreement. This collateral can be seized if the borrower fails to repay, adding an extra layer of security for the lender compared to a standard Promissory Note.

A Business Loan Agreement can also be compared to the Maine Promissory Note. This document is used when a business borrows money, outlining terms such as loan amount, interest rates, and repayment schedules. While the Promissory Note focuses on the borrower's promise, the Business Loan Agreement may include additional clauses related to business operations and financial reporting, making it more complex.

A Lease Agreement bears some resemblance to a Promissory Note in that both involve a promise to pay. In a Lease Agreement, a tenant agrees to pay rent to a landlord for the use of property. The terms of payment, duration, and conditions for termination are specified. Unlike a Promissory Note, which deals with loans, a Lease Agreement pertains specifically to rental arrangements.

When dealing with sensitive business information, it is essential to use legal documents like a Non-disclosure Agreement form to safeguard your interests. This type of agreement helps ensure that confidential details remain protected from unauthorized disclosure. If you are operating in Missouri and need to formalize the confidentiality of your information, consider using the Non-disclosure Agreement form to outline your obligations clearly.

An IOU is another document similar to a Promissory Note. An IOU is a simple acknowledgment of a debt. It states that one party owes a specific amount to another party. While it lacks the formal structure and legal enforceability of a Promissory Note, it serves as a basic record of a financial obligation. Both documents signify a debt, but an IOU is often less detailed.

Finally, a Credit Agreement is comparable to the Maine Promissory Note. This document outlines the terms under which credit is extended to a borrower. It includes details such as the credit limit, interest rates, and repayment terms. While a Promissory Note represents a single loan transaction, a Credit Agreement may cover multiple loans or lines of credit, providing a broader framework for borrowing.

Misconceptions

-

Misconception 1: A promissory note is only necessary for large loans.

This is not true. Promissory notes can be used for any amount of money, whether it's a small personal loan between friends or a significant mortgage. The key is that they provide a clear record of the loan terms, regardless of the amount involved.

-

Misconception 2: The Maine Promissory Note form is complicated and difficult to understand.

While legal documents can sometimes seem daunting, the Maine Promissory Note form is designed to be straightforward. It outlines essential information, such as the loan amount, interest rate, and repayment schedule, making it accessible for anyone to use.

-

Misconception 3: A promissory note does not require a signature.

In reality, a promissory note must be signed by the borrower to be valid. The signature signifies the borrower's agreement to the terms outlined in the document. Without a signature, the note lacks enforceability.

-

Misconception 4: Once a promissory note is signed, it cannot be changed.

This is misleading. While a signed promissory note represents a binding agreement, the parties involved can mutually agree to modify the terms. Any changes should be documented in writing and signed by both parties to avoid confusion later.

-

Misconception 5: Promissory notes are only for personal loans.

This misconception overlooks the versatility of promissory notes. They are commonly used in various contexts, including business transactions and real estate deals. Essentially, any scenario involving a loan can benefit from a promissory note to ensure clarity and legal protection.

Other Popular Maine Forms

Maine Homeschooling Laws - Indicate your educational philosophy through this letter to the district.

When seeking to confirm employment details, utilizing the Employment Verification Form is essential as it simplifies the process for both employers and financial institutions. This document not only streamlines the verification process but also ensures the integrity of the information presented by candidates. For those looking to quickly access this resource, you can find a comprehensive option at PDF Templates.

Rental Agreement Form Maine - This form should clearly state the property's address and included spaces.

Documents used along the form

When dealing with a Maine Promissory Note, several other forms and documents may be necessary to ensure a smooth transaction. Each of these documents serves a specific purpose and helps clarify the terms of the agreement between the parties involved. Below is a list of commonly used forms that accompany a Promissory Note.

- Loan Agreement: This document outlines the terms of the loan, including the interest rate, repayment schedule, and any collateral involved. It provides a comprehensive overview of the obligations of both the lender and borrower.

- Security Agreement: If the loan is secured by collateral, this agreement details the specific assets that back the loan. It protects the lender's interests in case of default.

- Trailer Bill of Sale Form: To properly document trailer ownership changes, refer to the comprehensive trailer bill of sale form resources for legal compliance.

- Personal Guarantee: This form is often used when an individual agrees to be personally responsible for the loan. It adds an extra layer of security for the lender.

- Disclosure Statement: This document informs the borrower about the terms of the loan, including any fees and the total cost of borrowing. It ensures transparency and helps borrowers make informed decisions.

- Amortization Schedule: This schedule breaks down each payment over the life of the loan, showing how much goes toward interest and how much reduces the principal. It helps borrowers understand their repayment obligations.

- Release of Liability: Once the loan is paid off, this document confirms that the borrower is no longer responsible for the debt. It provides peace of mind and clears any obligations related to the loan.

Having these documents prepared and understood can streamline the borrowing process and protect the interests of all parties involved. It is essential to ensure that each form is completed accurately to avoid any future disputes.

Form Preview Example

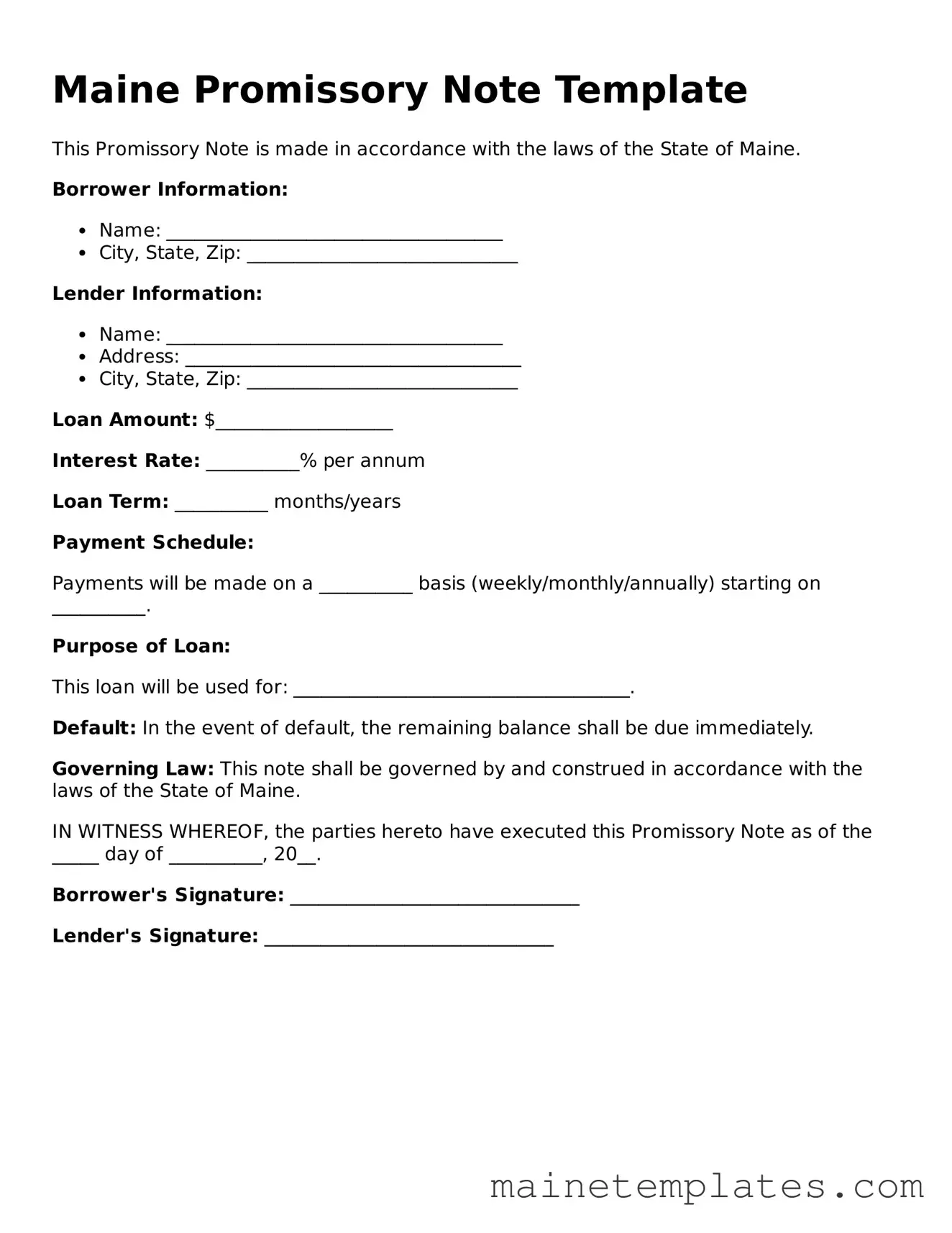

Maine Promissory Note Template

This Promissory Note is made in accordance with the laws of the State of Maine.

Borrower Information:

- Name: ____________________________________

- City, State, Zip: _____________________________

Lender Information:

- Name: ____________________________________

- Address: ____________________________________

- City, State, Zip: _____________________________

Loan Amount: $___________________

Interest Rate: __________% per annum

Loan Term: __________ months/years

Payment Schedule:

Payments will be made on a __________ basis (weekly/monthly/annually) starting on __________.

Purpose of Loan:

This loan will be used for: ____________________________________.

Default: In the event of default, the remaining balance shall be due immediately.

Governing Law: This note shall be governed by and construed in accordance with the laws of the State of Maine.

IN WITNESS WHEREOF, the parties hereto have executed this Promissory Note as of the _____ day of __________, 20__.

Borrower's Signature: _______________________________

Lender's Signature: _______________________________

File Information

| Fact Name | Description |

|---|---|

| Definition | A Maine Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a certain time. |

| Governing Law | The Maine Uniform Commercial Code (UCC) governs promissory notes in Maine. |

| Essential Elements | It must include the date, the amount to be paid, the interest rate (if any), and the signatures of the parties involved. |

| Types of Notes | Promissory notes can be secured or unsecured, depending on whether collateral is involved. |

| Enforceability | For a promissory note to be enforceable, it must meet the requirements set by the UCC and be signed by the borrower. |

| Default Consequences | If the borrower defaults, the lender may pursue legal action to recover the owed amount, including interest and fees. |

Detailed Guide for Using Maine Promissory Note

Once you have the Maine Promissory Note form in hand, it's important to complete it accurately to ensure that all terms are clear and enforceable. After filling out the form, both parties should retain copies for their records.

- Begin by entering the date at the top of the form. This is the date when the note is created.

- Next, fill in the name and address of the borrower. This identifies who is responsible for repaying the loan.

- Then, provide the name and address of the lender. This is the individual or entity that is providing the loan.

- Specify the principal amount of the loan. This is the total amount borrowed and should be clearly stated in both numerical and written form.

- Indicate the interest rate, if applicable. If there is no interest, you can leave this section blank or write "0%."

- State the repayment terms. This includes how often payments are due (e.g., monthly, quarterly) and the duration of the loan.

- Include any late fees or penalties for missed payments, if applicable. This helps clarify the consequences of not adhering to the payment schedule.

- Sign and date the form. The borrower must sign to acknowledge the terms, and the lender may also sign for verification.

- Finally, make copies of the completed form for both parties to keep for their records.